Why Transaction-Level Detection Breaks Under Structural Fraud

Raptorx.ai

Friday, May 22, 2026

Key Features:

- Explains why traditional transaction-level monitoring fails against modern, coordinated financial crime structures.

- Covers how structural fraud operates through connected accounts, devices, identities, and layered fund movement.

- Highlights the importance of relationship intelligence, behavioral context, and graph-based detection models in AML operations.

- Examines key operational challenges, including false positives, alert fatigue, and limited visibility in legacy monitoring systems.

- Explores the future of fraud detection through infrastructure-level risk analysis, explainability, and connected entity intelligence.

The Detection Gap Financial Institutions Can No Longer Ignore

For years, transaction monitoring has been the operational backbone of anti-money laundering and fraud detection programs. Most financial institutions built their controls around a straightforward assumption: suspicious activity can be identified by evaluating individual transactions against predefined risk indicators.

That assumption no longer reflects how modern financial crime operates.

Today’s fraud ecosystems are structured, coordinated, and intentionally fragmented across accounts, devices, channels, and jurisdictions. Criminal networks rarely depend on a single anomalous payment or a clearly suspicious transfer. Instead, they distribute activity across thousands of seemingly legitimate events designed to remain below traditional detection thresholds.

This creates a critical visibility problem for financial institutions.

A transaction may appear low-risk when viewed independently. But when connected to shared infrastructure, behavioral overlap, device reuse, beneficiary relationships, or coordinated movement patterns, that same transaction may represent one node inside a larger laundering or fraud operation.

This is where transaction-level detection begins to fail.

The issue is not simply that fraud has increased in volume. The structure of fraud itself has changed. Financial crime is now designed to exploit fragmented monitoring architectures that evaluate events in isolation rather than understanding the relationships between entities.

As regulatory expectations continue to rise and fraud networks become operationally sophisticated, institutions must rethink how detection systems interpret risk. The future of AML and fraud prevention will depend less on evaluating transactions individually and more on understanding the infrastructure connecting them.

The Original Purpose of Transaction-Level Detection

Existing transaction monitoring systems were designed during a period when financial crime patterns were comparatively linear and easier to isolate.

Detection models focused primarily on identifying:

- unusually large transactions,

- rapid movement of funds,

- geographic inconsistencies,

- abnormal withdrawal behavior,

- velocity spikes,

- sanctioned entities,

- and predefined typologies.

These systems typically rely on:

- static rules,

- threshold-based scoring,

- scenario monitoring,

- and historical alert logic.

For example:

- transactions exceeding predefined monetary thresholds,

- multiple transfers within a short timeframe,

- or payments originating from high-risk regions would trigger alerts for investigation.

This approach was operationally effective for conventional fraud patterns because suspicious behavior often appeared directly within the transaction itself.

However, modern financial crime rarely behaves that way anymore.

Criminal organizations now intentionally engineer activity to avoid transaction-level visibility.

The Structural Evolution of Financial Crime

Modern fraud operations increasingly resemble distributed financial infrastructures rather than isolated criminal acts.

Instead of relying on a single account or suspicious payment, fraud networks now operate through interconnected systems involving:

- mule accounts,

- synthetic identities,

- coordinated devices,

- layered payment chains,

- shell entities,

- account farms,

- and cross-platform transaction routing.

These networks are intentionally designed to fragment risk signals.

For example:

- One account may handle onboarding,

- another may receive deposits,

- Several may distribute funds,

- while separate devices and IP environments rotate activity to avoid behavioral consistency.

Individually, each activity appears legitimate.

Collectively, the infrastructure reveals coordinated criminal intent.

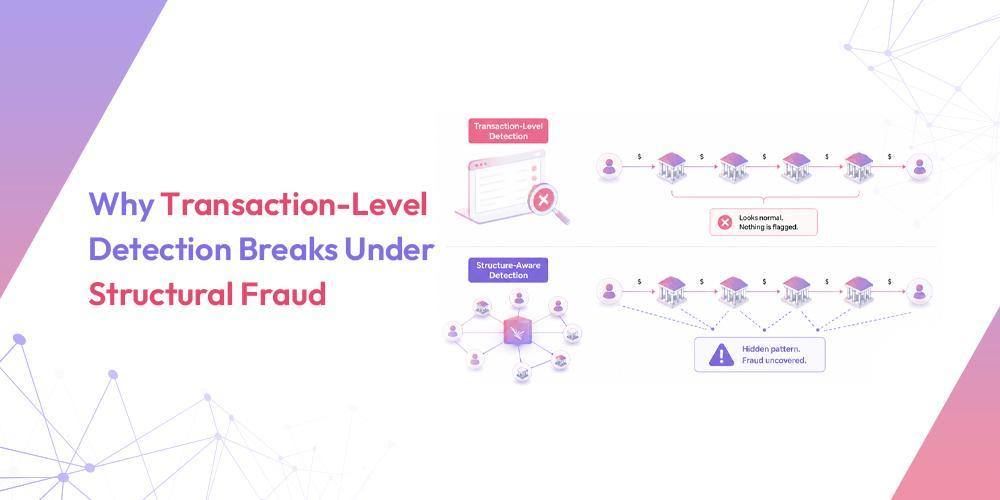

This operational model creates a major challenge for traditional monitoring systems because the suspicious signal no longer exists inside a single transaction. The risk emerges only when relationships between entities are analyzed together.

In many cases, no single transfer exceeds reporting thresholds, triggers scenario rules, or appears operationally abnormal.

The fraud exists in the structure itself.

Why Transaction-Level Detection Fails Under Structural Fraud

1. Transactions Do Not Reveal Relationship Intelligence

Transaction monitoring systems are fundamentally event-centric.

They evaluate:

- amounts,

- timing,

- geography,

- merchant behavior,

- or transactional velocity.

But structural fraud operates through relationships between entities.

The most important indicators frequently exist outside the transaction itself, including:

- shared devices,

- Repeated IP associations,

- linked beneficiaries,

- coordinated onboarding patterns,

- account reuse,

- or synchronized behavioral activity.

A payment may appear entirely normal in isolation. Yet the originating device may already be connected to dozens of previously flagged accounts.

Without relationship-level visibility, these hidden associations remain undetected.

This creates one of the largest structural weaknesses in conventional AML monitoring architectures.

2. Fraud Networks Intentionally Distribute Activity

Modern laundering and fraud operations deliberately fragment transactions to avoid triggering static controls.

Common structuring techniques include:

- low-value transaction splitting,

- staggered timing patterns,

- distributed wallet usage,

- rotating counterparties,

- and layered fund movement across multiple institutions.

Instead of transferring one large suspicious amount, networks may move hundreds or thousands of smaller transactions through intermediary accounts.

This reduces transaction-level anomaly visibility while preserving the operational objective of the criminal network.

From the perspective of traditional systems:

- each payment appears routine,

- each account appears low-risk,

- and each interaction independently falls within acceptable thresholds.

The structural pattern only becomes visible when activities are analyzed collectively over time.

3. Static Rules Cannot Adapt Fast Enough

Most legacy monitoring environments rely heavily on manually configured rules and threshold adjustments.

This creates operational rigidity.

Financial crime networks continuously adapt:

- transaction amounts,

- onboarding methods,

- behavioral timing,

- device usage,

- and channel selection.

Rule-based systems require ongoing recalibration to respond to these changes.

As fraud patterns evolve, institutions face a difficult tradeoff:

- Tighter controls increase false positives,

- looser controls increase missed detection risk.

This operational imbalance often produces alert inflation without materially improving investigative precision.

Over time, analysts become overwhelmed by high alert volumes while sophisticated fraud activity continues to bypass detection through structural fragmentation.

4. Lack of Behavioral Context Weakens Risk Interpretation

A transaction without context provides incomplete intelligence.

The same financial behavior can carry entirely different risk implications depending on:

- customer history,

- account maturity,

- device trust,

- peer-group behavior,

- onboarding characteristics,

- or linked entity activity.

For example:

- rapid outbound transfers from a newly established account connected to multiple previously flagged devices carry significantly different risk characteristics than similar activity from a long-established commercial account with stable historical behavior.

Transaction-only monitoring struggles to interpret this distinction because it evaluates events independently rather than contextually.

Modern financial crime increasingly exploits this gap.

5. Alert Volume Does Not Equal Detection Quality

One of the most persistent operational problems in AML and fraud operations is alert fatigue.

Traditional monitoring systems frequently generate excessive numbers of low-value alerts because threshold logic prioritizes sensitivity over contextual accuracy.

The result is:

- analyst overload,

- investigation delays,

- reduced operational efficiency,

- and increased risk of missing genuinely coordinated activity.

This creates a dangerous paradox: Institutions may generate more alerts while simultaneously reducing effective visibility into organized financial crime.

The issue is not a shortage of alerts.

The issue is insufficient precision in identifying structurally connected risk.

Structural Fraud Requires Infrastructure-Level Detection

Modern financial crime should no longer be viewed solely as a transaction problem.

It is an infrastructure problem.

Effective detection increasingly depends on understanding how entities interact across a broader operational environment.

This includes visibility into:

- account relationships,

- device associations,

- behavioral synchronization,

- payment pathways,

- identity overlap,

- network density,

- and risk propagation patterns.

The objective is no longer simply identifying suspicious transactions.

The objective is to identify suspicious systems of activity.

This shift fundamentally changes how risk must be interpreted inside financial institutions.

The Growing Importance of Graph-Based Detection Models

To address structural fraud, many institutions are moving toward graph-based investigation and detection frameworks.

Graph analytics focuses on relationships between entities rather than evaluating transactions independently.

These models help institutions identify:

- mule account clusters,

- synthetic identity networks,

- coordinated laundering activity,

- hidden intermediaries,

- circular fund movement,

- and shared operational infrastructure.

For example, graph analysis can reveal:

- multiple accounts connected through a common device,

- beneficiaries repeatedly interacting across unrelated customer groups,

- or transaction pathways designed to obscure fund origins.

These relationship structures are often invisible inside conventional transaction-monitoring workflows.

Graph-driven investigation models improve visibility into organized activity because they analyze how entities connect, evolve, and interact over time.

This becomes increasingly important as fraud networks grow more distributed and operationally sophisticated.

Why Explainability Matters in AML and Fraud Operations

As detection environments become more advanced, explainability becomes operationally critical.

Investigators, compliance teams, auditors, and regulators need clear reasoning behind elevated risk decisions.

Detection systems must provide:

- relationship transparency,

- investigative traceability,

- contextual evidence,

- and defensible escalation logic.

If analysts cannot understand why risk surfaced, operational trust declines.

Explainable detection improves:

- investigation speed,

- escalation confidence,

- regulatory defensibility,

- and operational consistency.

This is especially important in AML environments where institutions must justify:

- suspicious activity reports,

- customer risk classifications,

- account restrictions,

- and enhanced due diligence actions.

Visibility into relationship structures and behavioral reasoning is becoming just as important as the detection itself.

Real-Time Monitoring Alone Is Not Sufficient

Many modern fraud platforms emphasize real-time detection capabilities.

Speed is important.

But real-time transaction scoring alone does not solve structural visibility problems.

A system may analyze transactions instantly while still failing to identify:

- hidden relationships,

- coordinated networks,

- shared infrastructure,

- or distributed laundering behavior.

True modern detection requires:

- continuous relationship analysis,

- live network visibility,

- adaptive behavioral monitoring,

- and infrastructure-wide risk evaluation.

Without structural intelligence, faster transaction scoring simply accelerates incomplete analysis.

The Future of Financial Crime Detection

The future of AML and fraud prevention is shifting away from isolated event monitoring toward infrastructure-level intelligence.

Financial institutions increasingly require systems capable of:

- understanding entity relationships,

- identifying coordinated behavior,

- detecting emerging fraud structures,

- and adapting to evolving criminal methodologies.

This transition represents more than a technology upgrade.

It is a strategic shift in how financial crime itself is understood.

Institutions that continue relying primarily on transaction-level visibility will face growing operational blind spots as fraud networks become more interconnected and distributed.

The next generation of detection environments will be defined by:

- relationship intelligence,

- contextual risk analysis,

- explainability,

- operational adaptability,

- and structural visibility across financial ecosystems.

Conclusion

Transaction-level monitoring was built for a financial crime landscape that no longer exists.

Today’s fraud operations are coordinated, distributed, and structurally engineered to bypass isolated event analysis.

Modern criminal networks understand how traditional controls work. They intentionally fragment activity across accounts, devices, channels, and institutions to avoid triggering transactional anomalies.

As a result, suspicious activity increasingly appears legitimate when viewed one transaction at a time.

The core challenge facing financial institutions is no longer simply detecting abnormal transactions.

It is identifying hidden relationships, coordinated behavior, and interconnected financial infrastructure operating beneath seemingly ordinary activity.

This is why transaction-level detection breaks under structural fraud.

And it is why the future of AML and fraud prevention will belong to institutions capable of understanding not just transactions, but the systems connecting them.